You probably hear people talk about health insurance all the time. But you might feel like you don’t understand much about it. That’s OK, because, honestly, it can be a pretty confusing subject.

Like

most things, though, health insurance is something you can easily learn about

and master the basics. And that’s what Health Insurance 101 will help you

do.

So,

let’s look at a few questions together. What is health insurance, how does it

work? And should you get health insurance?

What Is Health Insurance?

Basically,

health insurance is a way of paying for your medical bills and health care

costs. Most people can’t pay for all their health care out-of-pocket, and just

put it on a debit or credit card.

Health

insurance can make it easier to pay your health care bills, and help you get

the care you need.

Different Kinds of Health

Insurance: Private and Government-run

There

are many different kinds of health insurance plans. Some plans are run by the

government. For example, you’ve probably heard of Medicare and Medicaid, which

are government-run:

- Medicare – health insurance for people age 65 and over, as well as some people under age 65 with a disability.

- Medicaid –

health insurance for people with a low income.

There

are also private health insurance plans. Many people get private health

insurance from their employer, and self-employed individuals often purchase

private health insurance, too. With private health insurance plans, you

typically pay the health insurer a monthly premium; with government-run health

insurance, there often is no monthly premium.

How Health Insurance Works

When

you have health insurance, your medical bills go first to your health insurance

plan. Then, they pay for some or all of that bill according to the plan’s details.

In

a way, health insurance is a lot like car insurance. If your car is in a bad

accident and needs a lot of work to repair it – or maybe it needs to be

replaced entirely with a new car – car insurance picks up some or all of the

cost. And that’s good, because the cost of fixing or replacing your car could

easily be more than you have in your bank account.

But,

unlike car insurance, health insurance covers far more than just the costs from

a bad accident. Health insurance often covers things like annual checkups,

vaccinations, preventive health and other “routine maintenance” for your body

and mind. It’s like if car insurance helped pay for oil changes and tire

rotations.

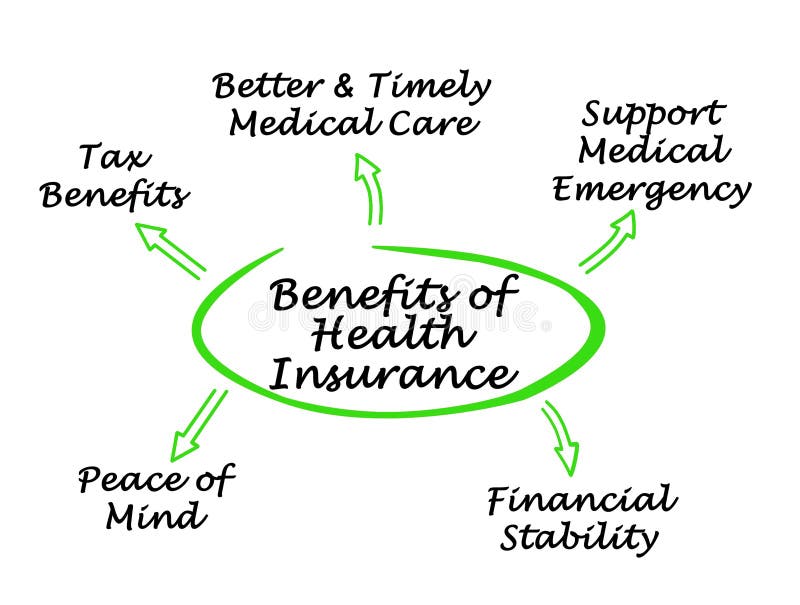

Why Should I Get Health

Insurance?

Broadly,

there are two reasons to have health insurance:

- Health insurance supports you if you get sick

- Health insurance helps you avoid getting sick to begin

with

Let’s

look at each of these reasons in more detail:

Health Insurance as a

Safety Net

It’s

important to have health insurance as a safety net. If you unexpectedly get

sick or injured, health insurance is there to help cover costs that you likely

can’t afford to pay on your own.

Health

care can be very expensive. It can be an enormous financial burden. Surgery,

emergency care, prescription drugs, lab work, scans and examinations – these

sorts of costs can add up very quickly. They can even be high enough to cause

individuals to go bankrupt, or to turn down care that they need but can’t

afford out-of-pocket.

But,

with health insurance, you’re not facing those costs as an individual; there’s

an insurance plan helping you cover the costs, and helping you navigate the

confusion of medical billing.

Let’s

face it, medical bills aren’t the sort of thing you want to be dealing with

while ill, injured, in a hospital bed or the emergency room. It’s smart to make

difficult financial decisions ahead of time, by getting health insurance before

you get sick.

Preventing Illness

The

other reason it’s important to have health insurance is that it makes it easier

for you to keep from getting sick in the first place.

Having

health insurance makes it easier for you to access – that is, find and pay for

– routine and preventive health care. This includes:

- Annual checkups

- Vaccinations (flu shots, MMR, etc.)

- Blood tests and lab work

- Scans and screenings

These

all play a role in keeping you healthy, and diagnosing any illness you might

have as soon as possible.

More,

health insurance helps cover the costs of managing any chronic conditions you

might have, such as diabetes, heart disease or depression. Health insurers

typically offer disease management programs for these kinds of conditions. They

can also point you to specialists and other resources that can help. That makes

it easier for you to keep on top of everything and stay healthy.

Routine

and preventive care is especially important where children are concerned. Kids,

infants and pregnant mothers all need regular medical care to keep them healthy

and thriving. Early intervention prevents problems down the road, and can even

save lives.

And

it isn’t just about physical health: health insurance typically covers mental

and behavioral health care, as well.

Can I Afford Health

Insurance?

To

sign up for a private health insurance plan, you typically have to pay a

monthly premium. It’s far more likely that you can afford health insurance than

that you can afford to pay for a surgery, illness or emergency room visit out

of your own pocket.

Private

health insurers usually offer a variety of plans with different premiums in

order to reach a wide range of income levels.

If you can’t afford a private health

insurance plan, you might be eligible for a government health insurance plan,

such as Medicaid or Medicare. Or you might be eligible for subsidies (i.e.,

financial support) on the healthcare.gov Health Insurance Marketplace.

Cost-sharing

Health

insurance doesn’t cover everything, though. Apart from paying your monthly

premium, there are several forms of cost-sharing in most insurance plans. We’ll

go over them below and explain how they work.

First there’s the deductible, which is the amount of health care costs

you have to pay for before the insurance plan starts sharing those costs. So,

if your plan’s deductible is $1,000, then you have to cover the first $1,000 of

medical costs before your health insurance plan begins picking up its share of

the bill.

Insurance plans often have you pay a copay when you see a doctor. There can also be

a coinsurance arrangement where, for example, you

pay 20% for some medical bills and the insurance plan picks up the other 80%.

Copays and coinsurance typically come into play after you’ve met your

deductible (though sometimes they’re at work even before you’ve spent that

amount).

Finally, there is the out-of-pocket maximum (or maximum out-of-pocket).

That’s the amount of money that, once you’ve spent it on health care costs in

any year, the health insurance plan pays for 100% percent of your health care

bills. All you pay is your monthly premium.

Here’s

an example of how it works with numbers plugged in. We’ll call it the “Ten

Plan”, and keep the number simple.

Ten Plan (example)

- $10 Copay (after deductible met)

- 10% Coinsurance (after deductible met)

- $1,000 Deductible

- $10,000 Out-of-pocket maximum

So,

in the Ten Plan, apart from paying your monthly premium, you’re going to pay

out of pocket for the first $1,000 of your health care costs (i.e., your

deductible). That includes doctor visits, lab work, x-rays, surgery, physical

therapy, everything. After that, though, you’ll only pay $10 per doctor visit,

and only pay 10% of other health care costs.

And,

if you wind up spending $10,000 altogether in a given year, your health insurance

plan picks up the cost of everything for the rest of the year. All you pay is

your monthly premium.

What If I Don’t Get Sick?

Don’t I Lose Money?

You

might be wondering, “If I sign up for health insurance, pay my monthly premium,

but I don’t get sick and don’t get any health care, then I’ve lost money.”

That’s

not quite right, though.

First,

there are many health insurance benefits you can use even without getting sick,

such as vaccinations and checkups, that help keep you healthy over the long

run.

Second,

even if you don’t get into an accident, have large health care costs, or need

to use your health insurance benefits, you still get the peace of mind of

knowing that, if you had gotten sick, you wouldn’t be facing all those medical

costs on your own.

Last,

even when you don’t use your own health insurance benefits, your premiums go to

pay for the benefits and health care of others on your plan. And, some day,

when you do get sick and need help paying your medical bills, the others on

your plan will help you in the same way.